Loan Amortization Schedules: A Beginner's Guide to Saving Money

Loan amortization schedules are essential tools that can significantly enhance your understanding of loan payments. By breaking down each payment into principal and interest, these schedules allow borrowers to visualize their repayment journey. A comprehensive grasp of amortization not only aids in managing debts but can also lead to potential savings over the life of the loan.

As a beginner in the financial landscape, comprehending loan amortization schedules can provide a solid foundation for making informed borrowing decisions. Whether you are looking to purchase a home, finance a car, or consolidate debt, knowing how amortization works can equip you with the necessary knowledge to navigate your financial obligations. This guide will delve into the intricacies of loan amortization, exploring its importance, types, and practical application.

Understanding loan amortization will ultimately empower you to take control of your financial future, improve your budgeting skills, and identify strategies for saving money. Let's dive deeper into this essential aspect of loans and discover how it can work in your favor.

What is Loan Amortization?

Loan amortization refers to the process of gradually paying off a debt over time through a series of fixed payments. Each payment consists of both principal and interest components, with the goal of paying off the entire loan by its maturity date. The breakdown of these payments changes throughout the loan term, with early payments consisting primarily of interest and later payments focusing more on the principal balance.

Amortization schedules are typically used for various types of loans, including mortgages, car loans, and personal loans. They provide borrowers with a detailed outline of each payment, allowing them to see how much of their payment goes toward reducing the loan's principal and how much goes toward interest. This transparency is invaluable as it allows borrowers to strategize their financial decisions more effectively.

Understanding the concept of amortization is crucial for anyone looking to take on a loan. It not only helps in calculating monthly payments but also aids in planning ahead for future financial commitments.

Why is Amortization Important?

Amortization is important because it provides a structured repayment plan for loans, ensuring that borrowers understand their financial obligations over time.

- Ensures timely repayment of loan principal and interest

- Helps borrowers budget their finances effectively

- Provides insight into the remaining balance over time

These aspects create a clearer financial picture, making it easier to manage debts and prevent falling into financial distress. Understanding amortization can also empower borrowers to make informed decisions, such as when to refinance or pay off loans early.

Types of Loan Amortization

Loan amortization can come in various forms, each with its own structure and repayment plan. The type of amortization chosen can significantly affect the total cost of the loan and the monthly payment. Understanding the different types of loan amortization will help borrowers choose the best option for their financial situation and needs.

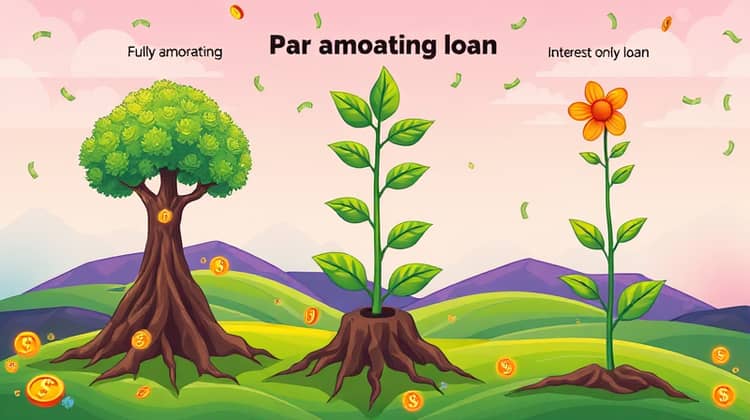

At its core, loan amortization can be categorized into fully amortizing, partially amortizing, and interest-only loans. Knowing the differences and implications of each type can illuminate the best path for responsible borrowing and repayment.

Choosing the correct type of loan amortization is crucial to managing your finances effectively and avoiding pitfalls associated with excessive debt.

1. Fully Amortizing Loans

Fully amortizing loans require borrowers to make consistent monthly payments that will pay off the entire loan balance by the end of the loan term.

- The payment amount remains the same throughout the loan term

- Interest is computed on the remaining balance

- By the end of the term, the loan is completely paid off

This structure offers predictability and stability for borrowers, making it easier to budget monthly expenses. Fully amortizing loans are highly popular for mortgages.

2. Partially Amortizing Loans

Partially amortizing loans require borrowers to make payments that do not fully cover the principal by the end of the loan term.

- At the end of the term, a balloon payment is required to settle the remaining balance

- Monthly payments consist of both principal and interest, but not enough to amortize the loan entirely

- This type can provide lower initial payments, but carries the risk of larger payments in the future.

Borrowers should be cautious with partially amortizing loans, as the balloon payment can come unexpectedly and strain finances.

3. Interest-Only Loans

Interest-only loans allow borrowers to pay only the interest for a specified period, typically 5-10 years, without reducing the principal.

- Lower initial payments can enhance cash flow during the interest-only period

- After the interest-only period, payments switch to fully amortizing, increasing significantly

- These loans can be risky if borrowers do not plan for the higher payments that will follow.

Interest-only loans may be attractive for some borrowers, but they require careful planning and budgeting to ensure they can handle the eventual repayment of the principal.

How Loan Amortization Schedules Work

Loan amortization schedules outline the payment structure of a loan over its term. Each payment is broken down into principal and interest components, illustrating how both change over time as the loan decreases.

As borrowers make payments, a portion of the payment reduces the principal, while another portion covers the interest accrued. A typical amortization schedule will start with payments that are heavily weighted toward interest and gradually shift to primarily reduce the principal.

Understanding how these schedules work can provide valuable insights into the cost of borrowing and the implications of making additional payments toward the principal.

Benefits of Using an Amortization Schedule

Using an amortization schedule offers several benefits to borrowers.

- Provides a clear picture of total interest paid over the life of the loan

- Helps in budgeting monthly expenses accurately

- Allows borrowers to track progress in paying off the loan

By utilizing an amortization schedule, borrowers can make more informed financial decisions and manage their loans more efficiently. This practice can lead to significant savings over time and help maintain a healthy credit profile.

How to Read an Amortization Schedule

Reading an amortization schedule might seem daunting at first, but understanding its structure is essential. An amortization schedule typically includes columns for payment number, payment amount, interest component, principal component, and remaining balance.

The first few rows of the schedule will reveal how much interest is being paid initially, and as you move down the schedule, you will notice the shifting balance toward principal payments. Knowing this information empowers borrowers to manage their finances more proactively and take control of their repayment.

Familiarizing yourself with these details can help in making critical decisions regarding additional payments or refinancing options, ultimately enhancing your financial literacy.

DIY Amortization Schedules vs. Online Calculators

Creating a DIY amortization schedule can provide a better understanding of payments, but online calculators simplify the process. Both methods have their merits and can be beneficial depending on the situation.

DIY schedules offer personalized insights and the opportunity to create customized loan terms. However, they can be time-consuming and require careful calculations that may lead to mistakes without proper tools.

Online calculators, on the other hand, are convenient and often provide rapid results without the hassle of manual calculations. They can quickly generate schedules and can be particularly useful for comparing different loan options.

Ultimately, the choice between a DIY schedule and an online calculator depends on personal preference and financial goals. Both can play a role in improving your understanding of loan amortization.

Tips for Saving Money with Loan Amortization

Saving money with loan amortization is not just about making regular payments. There are strategic approaches that can lead to significant savings over the loan term.

- Make extra payments toward the principal whenever possible

- Refinance your loan to secure a lower interest rate

- Consider making bi-weekly payments instead of monthly

By implementing these strategies, borrowers can reduce the overall interest paid over the length of their loans and even shorten the loan term. Such proactive measures can lead to better financial health and help achieve long-term goals more efficiently.

Conclusion

In conclusion, understanding loan amortization and the related schedules is pivotal for anyone looking to navigate their borrowing options effectively. The knowledge gained from these schedules can enlighten borrowers on their financial commitments and help them make more informed decisions.

Loan amortization not only plays a significant role in determining the overall cost of borrowing but also aids in budgeting and financial planning. By taking control of repayment schedules and recognizing potential savings strategies, borrowers can enhance their financial futures.

Ultimately, knowledge is power. Armed with a comprehensive understanding of loan amortization, borrowers can approach their loans with confidence, ensuring they make choices that will serve them well now and in the long term.