Annuities in Retirement Planning: A Simplified Guide for Secure Finances

In today's increasingly complex financial landscape, securing a stable income in retirement is paramount. This guide will simplify the concept of annuities and their role in retirement planning, presented in manageable sections to enhance understanding.

An annuity can serve as a financial safety net, allowing retirees to enjoy their golden years without stressing over income fluctuations. We'll explore various types of annuities, how they function, their pros and cons, and valuable tips for purchasing one.

What is an Annuity?

An annuity is a financial product that provides a stream of income over a specified period, often designed for retirees. It is typically purchased from a financial institution such as an insurance company, where the individual pays a lump sum or makes a series of payments in exchange for guaranteed periodic payments in the future.

Annuities can be a vital part of a retirement strategy, offering predictable income sources and the potential for growth, depending on the type chosen. They can help mitigate the risk of outliving one’s savings, offering a sense of security in an uncertain financial future.

Types of Annuities

When considering annuities, it's essential to know that they come in various forms, each serving different financial needs and goals. Understanding these types can help individuals align their choices with their retirement plans, maximizing their benefits.

Here are a few common types of annuities to consider:

- Fixed Annuities: Provide a guaranteed return and predictable income stream.

- Variable Annuities: Offer investment options and returns based on market performance, with income varying accordingly.

- Indexed Annuities: Combine features of both fixed and variable annuities, linking returns to a stock market index.

With a range of options available, choosing the right type requires careful consideration of personal financial situations and retirement goals. Understanding the differences can guide informed decisions.

Immediate vs. Deferred Annuities

Annuities can also be categorized based on when the payments begin. Immediate annuities start providing income right away, while deferred annuities accumulate value before payments commence.

Choosing between immediate or deferred annuities typically depends on an individual’s financial station and requirements at retirement. Immediate annuities may suit those who need quick access to income, while deferred annuities can be beneficial for growth strategies.

- Immediate Annuities: Payments begin almost immediately after purchase.

- Deferred Annuities: Payments start at a later date, primarily used for long-term growth.

Selecting the right timing for payments is critical in aligning the annuity with personal retirement funding strategies.

Fixed vs. Variable Annuities

Understanding the differences between fixed and variable annuities is essential, as these options have distinct implications for risk and return. A fixed annuity offers predictable returns and is suitable for conservative investors seeking stability.

Conversely, a variable annuity enables the holder to choose investment options, which can lead to higher returns but also come with increased risks associated with market fluctuations.

- Fixed Annuities: Offer guaranteed interest rates and income.

- Variable Annuities: Returns are subject to market performance and investment choices.

Choosing between fixed and variable annuities involves understanding your risk tolerance and income needs.

Why Consider Annuities in Retirement Planning?

Annuities play a significant role in retirement planning for several reasons. They provide a steady income stream, which is crucial for retirees who want to cover their essential expenses without the stress of market volatility.

Moreover, annuities can offer tax-deferred growth, allowing individuals to accumulate savings without immediate tax implications, maximizing their investment potential over time.

- Predictable income stream in retirement

- Protection from market fluctuations

- Possibility of lifetime income options

- Potential tax advantages

Given their multiple advantages, annuities can complement other retirement income sources, enhancing financial security.

How Annuities Work

Annuities function based on a straightforward premise: individuals pay a sum of money to an insurance company or financial institution, which then promises to pay back a steady stream of income over a period. The payouts can start immediately or after a certain accumulation period.

The amount received as payments depends on factors like the type of annuity, the chosen payout period, and the initial investment. Understanding these mechanics is critical for effective financial planning.

- Purchase an annuity through an insurance provider or financial institution.

- Decide on the payment type - lump sum or installments.

- Choose between immediate or deferred income payouts.

- Select fixed or variable options based on preference.

Grasping these operational elements aids in making informed and strategic decisions about annuities in one's retirement plan.

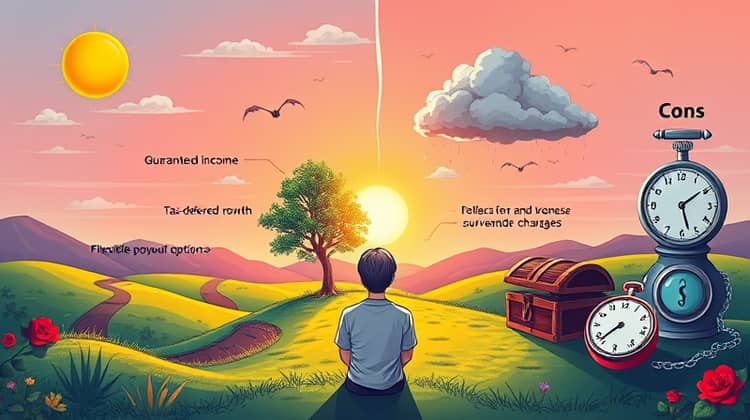

Pros and Cons of Annuities

Annuities can be valuable tools in retirement planning but come with both advantages and disadvantages. Understanding these facets allows individuals to evaluate whether they align with their financial goals.

Below are some pros and cons to consider for annuities:

- Pros: Guaranteed income, tax-deferred growth, flexible payout options, and potential lifetime income.

- Cons: Fees and expenses, less liquidity, and surrender charges if accessed early.

Considering both sides can assist in making a balanced decision about including annuities in an overall retirement plan.

Who Should Consider An Annuity?

Annuities can be attractive for various individuals, particularly those seeking stable income sources during retirement. They are especially suited for early retirees or those with limited savings who desire a predictable cash flow.

Additionally, individuals concerned about outliving their savings may find annuities a wise choice, offering peace of mind against financial uncertainties.

- Retirees seeking reliable income flow

- Individuals wanting to reduce market risk

- Those interested in tax-deferred growth

- Anyone concerned about longevity risk

Identifying personal financial situations can help determine if annuities should be a component of one's retirement strategy.

How to Buy an Annuity

Purchasing an annuity involves several key steps, ensuring that individuals make informed decisions aligning with their financial goals. It's essential to research and compare various products before making a commitment.

Here’s a concise guide on how to buy an annuity:

- Evaluate your financial situation and retirement needs.

- Research different types of annuities available.

- Contact a licensed insurance agent or financial advisor for detailed options.

- Compare fee structures, payouts, and terms.

- Make an informed decision and complete the paperwork with the chosen provider.

A thorough approach to purchasing annuities can lead to effective financial planning and secure future income.

Conclusion

In conclusion, annuities can provide a robust solution for individuals looking to secure their financial future during retirement. Understanding their functions, benefits, and drawbacks is essential for aligning annuities with personal retirement goals.

With proper planning and consideration, annuities can offer peace of mind, ensuring steady income flow and protection against market risks, ultimately enhancing the quality of life in retirement.